Bradley Hall saw sales and lettings continue to stand firm during the first quarter of 2023, despite the economic uncertainty which buffeted the market.

In this report, we break down the most significant deals completed during the quarter, as well as taking a look at the kinds of deals and property that piqued the interest of investors most.

We also outline our predictions for the market as we head into the second quarter, which – if early indicators are a sign of things to come - will offer opportunities aplenty for astute investors.

“Confidence in the North East property market remains high. It’s been a tough period for both people and businesses alike, but we’re finding that people still see the region as a great place to invest and there remains plenty of great commercial opportunities for those seeking to capitalise on falling prices and fantastic one off opportunities.” – Richard Rafique, Managing Director – Commercial

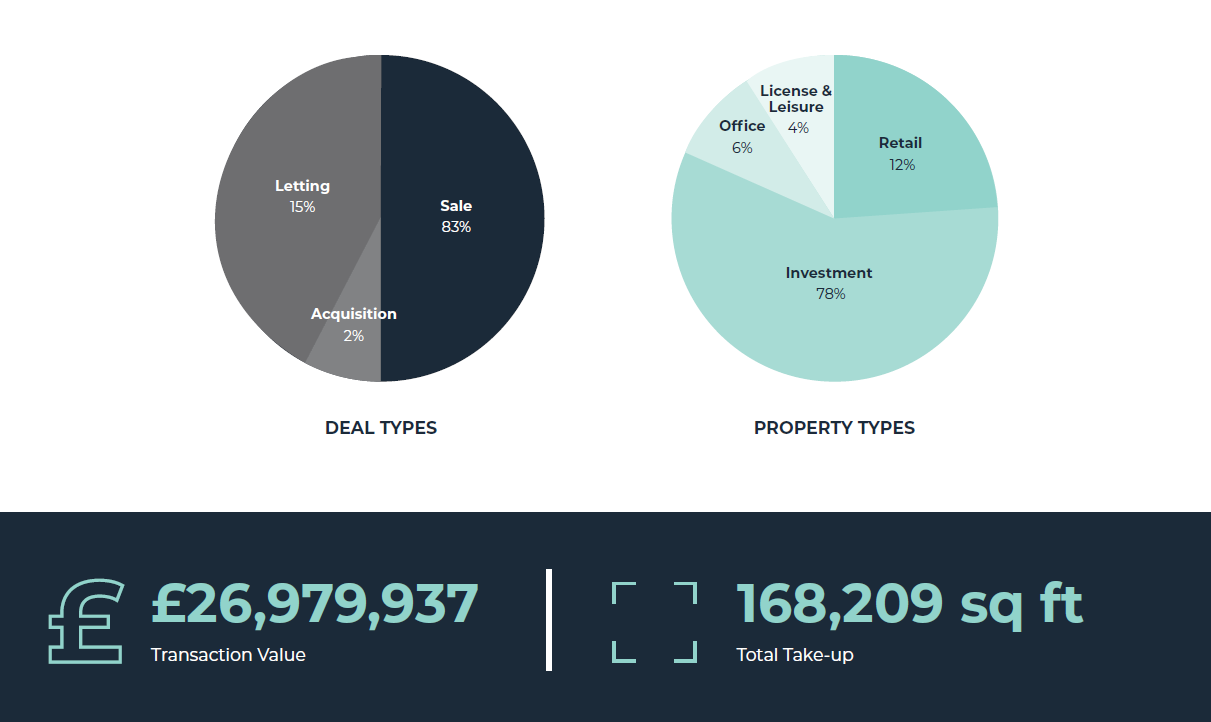

Bradley Hall – Q1 Breakdown

Retail

Newcastle’s retail market is rebalancing after the initial effects of the pandemic, which caused the amount of vacant floorspace to roughly treble in 18 months.

Shopping centres have also been hit hard, though tenant demand has revived since restrictions were lifted. Flannels and Sports Direct exchanged contracts to lease 70,000 SF and 60,000 SF, respectively, within the former Debenhams store at the Metrocentre’s Red Mall in Q3 2022. The agreements follow Harrods HBeauty, JD Sports and H&M expanding into over 80,000 SF at the mall, which is among Europe’s largest, in Q2. Swatch, iSmash, The Real Greek and Be More Geek occupied a total of 20,000 SF at Eldon Square, the market’s other main shopping centre, earlier in Q1.

The growth of discount grocers, which typically gain market share during downturns, represents another bright spot for demand. The Food Warehouse opened a 10,000-SF store at Westmorland Retail Park, Cramlington, in Q3 2022, while Heron Foods began trading from 187–193 Durham Road, Gateshead, earlier in the year. The 6,700-SF store is the B&M-owned retailer’s fourth in Gateshead. It has around 40 across the wider Newcastle market.

Aldi will soon open a 14,000-SF outlet at Kingston Retail Park, having opened a 19,000-SF supermarket in Bedlington in late 2021. Lidl’s most recent site requirements list outlines 30 or so locations in the North East of England, including seven in Newcastle, four in Gateshead and two in Sunderland.

After two relatively strong years, retail investment in Newcastle has begun to moderate. Sales volumes have amounted to £96.2 million over the past 12 months, which compares to a five-year annual average of £158 million. Average yields have moved out to 8.0%, reflecting the weaker occupational landscape since COVID-19, the cost-of-living crisis and higher interest rates.

Investor demand for shopping centres and high street retail assets has picked up somewhat amid softer pricing. The Reuben Brothers’ Motcomb Estates added to its Newcastle city centre holdings in October after purchasing the Central Exchange leisure and shopping arcade for around £11.7 million. The deal is understood to have reflected a net initial yield north of 8% and a reversionary yield above 9%. Also in October, a private investor acquired Gosforth Shopping Centre at £9.3m.

The sale of a Primark store in Newcastle city centre remains one of the largest single-tenant investment deals of the past 18 months. John Berk acquired the 84,000-SF property at 78–92 Northumberland Street from Arioso AG for £13.8 million.

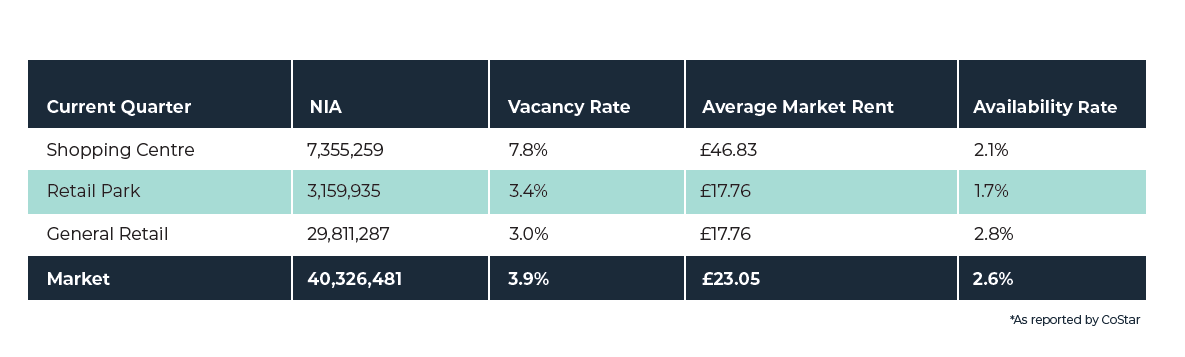

Regional sector performance as reported by CoStar:

Deals: 125 Value: £146,000,000

The top retail deals completed by Bradley Hall during the first quarter of 2023:

7-8 Pennywell Shopping Centre

Price: £12,000.00

Size: 664 sq ft

Deal: Letting

Client: Private Individual

Osborne Road

Price: £17,000.00

Size: 664 sq ft

Deal: Letting

Client: Swan Residential Lettings Ltd

Industrial

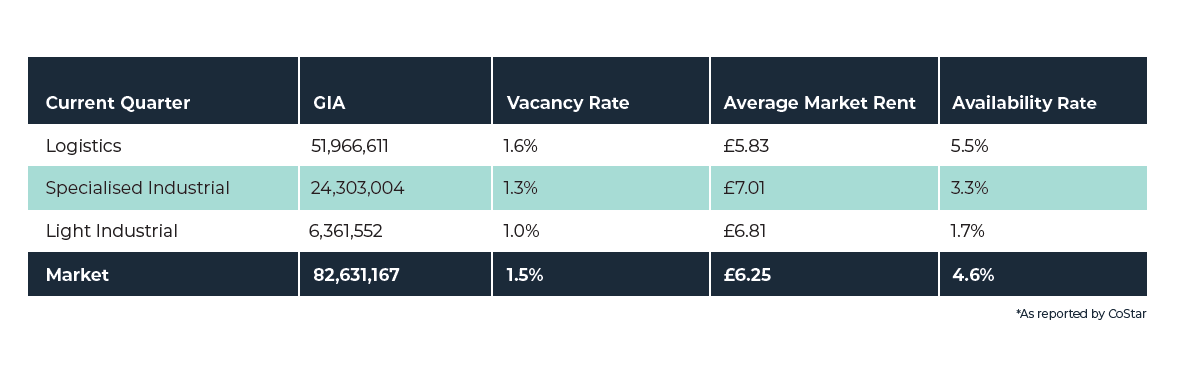

Newcastle’s industrial landlords are enjoying the tightest market conditions ever recorded. Demand has outweighed supply in all but one of the past seven years, with vacancies down at 2.0%, the lowest rate in nearly 15 years.

Prime distribution warehouse rents in Newcastle stand around £7/SF, with top rents in smaller warehouses north of £8/SF, according to local market participants.

Looking ahead, while rent growth is expected to slow, one factor that could support rental values in certain locations is the fact that rent accounts for a relatively small portion of logistics occupiers’ operating costs (less than 5%). Some occupiers might therefore be inclined to pay higher rents if they can offset rising transport costs, which typically account for over 50% of operating expenses, by reorganising their distribution network.

Obsolescence is perhaps the major downside risk facing local industrial owners. The North East of England has some of the nation’s oldest warehouse stock, alongside Scotland and Wales. Nearly three-quarters of the region’s industrial inventory, equivalent to 110 million SF, was built last century. About 25% of buildings predate 1980. The median time older and larger facilities (pre-1980 and 100,000 SF-plus) spend on the market has been increasing lately to stand at 27 months as of March 2023. Without investment by landlords, many of these buildings will be unlettable by 2025 when all newly rented properties will be required to have an EPC rating of C or above.

Office

Newcastle’s office vacancy rate is rising after a period of relative stability. Like other office markets across the country, demand is polarised between the best-quality offices with strong ESG credentials and older stock lacking sustainability and wellness features.

HMRC’s commitment to a 460,000-SF regional hub at Pilgrim’s Quarter has boosted confidence in the city centre office market, while demand is holding up relatively well out-of-town.

Although construction has picked up, the speculative schemes underway had about 200,000 SF available in early 2023. Bank House will help to alleviate availability constraints in Newcastle City Core, while Sunderland is set to benefit from the Faber and Maker buildings. Insurance giant RSA pre-let 37,000 SF at the former in Q2 2022. The next major scheme to come forward is likely to be The Pioneer, a 100,000-SF wellness-oriented building within the emerging Stephenson Quarter.

Regional sector performance as reported by CoStar:

Deals: 68 Value: £84,500,000

The top office deals completed by Bradley Hall during the first quarter of 2023

Linnet Court, Alnwick

Price: £37,025.00

Size: 2,475 sq ft

Deal: Letting

Client: Northumberland Estates

Esh Space, Bowburn North Industrial Estate, Durham

Size: 4,635 sq ft

Deal: Sale

Client: Esh Group

5 Saville Place

Price: £7,500.00

Size: 461 sq ft

Deal: Letting

Client: Greenbow Properties Limited

Investment

Across the North East softer pricing has brought some buyers back to the table for shopping centres and properties on the high street. Retail warehouses let to discounters and food stores remain favoured for the perceived defensiveness in the current climate. Subdued trading is expected in the months ahead, however, given the cost-of-living squeeze and rising interest rates.

The top investment deals completed by Bradley Hall during the first quarter of 2023:

1-3 Beaumont Street, Hexham

Price: £837,500.00

Size: 12,141 sq ft

Deal: Sale

Client: Administrators

NIY: Yield - 7.62%

19-20 Blandford Street

Price: £775,000.00

Size: 5,349 sq ft

Deal: Sale

Client: Private Individual

NIY: Yield - 8.04%

Licensed and Leisure

Preliminary January results, however, show that the city may not be experiencing any slowdown yet, further pointing to the hospitality industry’s resilience, as consumers continue to favour experiences. RePAR is due to improve on 2019 levels by 14% in January as occupancy and rates outperform such levels.

Comprising 8,400 rooms, it is a well-supplied and condensed hotel market for its size. Over the past decade, the market saw significant additions to new supply, especially between 2011 and 2018, when new room growth amounted to approximately 5% annually, ahead of the 1% national average. During the period, some sizeable properties opened with over 200 room, with the largest addition to the market being the Maldron Hotel Newcastle with 265 rooms, opened in 2018.

New room supply is not expected until 2024 but will be significant, with one dual-branded project underway- the ibis and Novotel Newcastle Gateshead Quays-adding 327 rooms.

Regional sector performance as reported by CoStar:

Deals: 68 Value: £84,500,000

The top office deals completed by Bradley Hall during the first quarter of 2023:

Unit 1 Keel Square, Sunderland

Size: 9,036 sq ft

Deal: Letting

Client: Sunderland City Council

The Links Hotel, Seahouses

Size: 5,899 sq ft

Deal: Acquisition

Client: The Inn Collection Group

The Carlton Lodge Hotel, Helmsley

Size: 4,542 sq ft

Deal: Acquisition

Client: The Inn Collection Group

Sign up to our mailing lists to stay up to date with the latest news here