Welcome to the third quarterly Leeds Commercial Property Review of 2023 by Bradley Hall. The analysis will provide you with an in-depth overview of the city’s commercial property market, helping you to make more informed decisions when making your next investment and when planning for the future.

“The area’s thriving advanced manufacturing and logistics industries, coupled with its growing reputation as a financial and professional services hub, has led to Leeds’ commercial property sector continuing to thrive over recent months, with investor confidence remaining above the UK average. Industrial vacancy rates are below the national average, with new and refurbished space being popular in recent months among occupiers. Units with strong sustainability credentials have also proved popular.” -David Cran, Managing Director, Bradley Hall Yorkshire and North West.

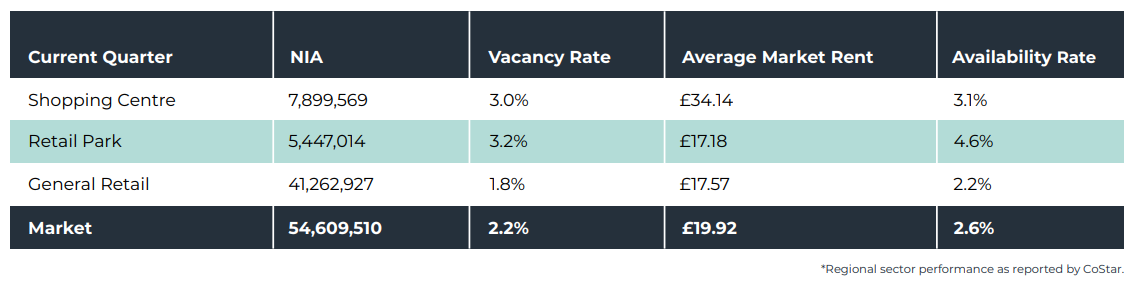

Retail

Leeds’s retail market comprises the metropolitan county of West Yorkshire, the second most populous urban area in northern England and one of the largest in the UK, with a population of 2.4 million. Its substantial size and buying power potential make it one of the nation’s most important retail centres. Leeds is home to 54.6 million SF of retail space, equating to about 22 SF per capita, which is in line with the UK national average.

The effects of the pandemic and the cost-of-living crisis on Leeds’s retail market are expected to linger. Retail and recreation footfall in Leeds was still down around 10% on its pre-coronavirus baseline in October, which was broadly in line with Manchester but a stronger recovery than London (-21%), according to Google’s mobility trends. Another headwind facing retailers is persistently high inflation, which is dampening consumers’ propensity to spend (the GfK Consumer Confidence indicator remains near its historic low at -45 in January 2023).

Leeds’s retailing environment has softened since the pandemic, with annual net absorption flat and the vacancy rate trending upwards, albeit it remains at a low level. Notable store closures include Debenhams, Topshop and the Disney store, all at the White Rose Shopping Centre; Debenhams on Briggate, Timberland on Albion Street and Thorntons on Commercial Street, all in the city centre; and Peacocks at Kirkstall Bridge Shopping Park.

Discount and value retailers have been involved in most of the larger new openings over the past 12 months. Most recently Primark has taken 55,000 SF at the Broadway Bradford – at the store formerly occupied by Debenhams, which has been vacant since 2021. They will be relocating from the nearby Kirkgate Store after Bradford Council bought the Kirkgate Centre with a view to repurposing the site in the coming years. Other examples include The Range taking 46,500 SF at Pellon Lane, Halifax, Dunelm taking 18,300 SF at The Springs in Leeds and Easy Bathrooms taking 20,000 SF at Beck Retail Park in Wakefield.

Property owners are also looking to repurpose vacant space. In January, Gravity Entertainment signed 23,000 SF at Xscape in Wakefield and Nuffield Health took 38,000 SF at Otley Road in Bradford.

Investment activity has slowed in recent months as interest rates and debt costs have soared. Several shopping centres changed hands in early 2022 – most notably Leeds Victoria Gate and Victoria Quarter – albeit at prices well below what they were once worth. HIG Capital and Bride Hall Group sold Kirkgate Shopping Centre, Bradford to the City of Bradford District Council for £15.5m reflecting a net initial yield of 9%. Market sources report that its acquisition and subsequent demolition will enable the council to double the size of its plans for a new urban village, including 1,000 homes.

In August Frasers Group bought the former Debenhams Store on Briggate, Leeds for £40 million from Orchard Street Investment Management. Earlier in the year, buyers were showing a strong preference for retail assets perceived to be defensive such as supermarkets and retail warehouses tenanted by “essential” retailers, although this activity has slowed given the current slowdown. Average yields have moved sharply outwards over the past couple of years amid the structural shift in shopping patterns and uncertain occupational backdrop.

Industrial

Leeds hosts one of the UK’s largest and most dynamic industrial markets, aided partly by its links to the M62 and M1 motorways. As well as

serving as a key logistics hub, it is home to one of the UK’s largest clusters of manufacturing businesses, which generate around 12% of the

City Region’s economic output. Significant warehouse occupiers in Leeds include Amazon, Marks & Spencer, Coca-Cola and The Range.

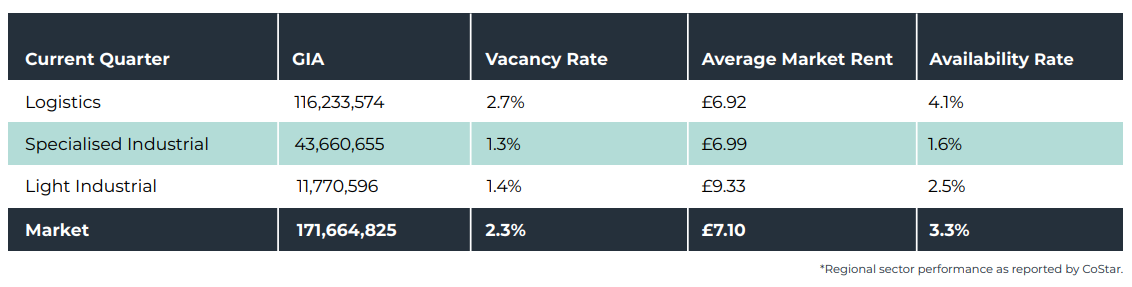

Industrial occupier market conditions in Leeds have fallen back from the heady levels of the past few years. That said, the vacancy rate is currently at 2.3% having trended below the UK national average since 2015 and is the lowest of the nation’s industrial markets with 100 million SF of stock or more.

New and refurbished space has been popular in recent months among occupiers. Melburg Capital has recently prelet 210,000 SF Voltaic, Wakefield 41 to XPO Logistics, which is currently under refurbishment. Although with the slowdown in online spending, recent months have been dominated by mid-box activity, which has replaced big-box lettings by the likes of Amazon, Next and Easy Bathrooms, agreed during the pandemic. New units at Overland Park on the M62 have strong sustainability credentials and have let successfully in recent months, to occupiers such as A Leadbeater Transport (65,755 SF) and Vintage Cash Cow (38,990 SF).

Fuelled by rising but historically low vacancies, average industrial rent growth in Leeds is running well above its historical average (3.8%) at an annualised growth rate of 6.3%. In the Base Case forecast, further strong rent growth is expected in the near term, although the pace of growth is expected to continue tapering (from a peak of 9.9% in Q1 2022) but remain comfortably positive.

Investment volumes over the past 12 months have amounted to £202 million, having fallen back in recent quarters as interest rates and debt costs increased. This compares to a five-year rolling annual average of £458 million. Recent months have seen an improvement in activity compared to the beginning of 2023, with a variety of deals including portfolio activity, sale and leaseback, asset management opportunities and deals with good covenants and long leases. A recent transaction in September involved the sale of an owner-occupied warehouse. Pan-European urban logistics platform Crossbay purchased 168,800-SF Shawcross 170 in Dewsbury from Nobia UK for £13.6 million from Rixonway Kitchens, who had occupied the building since construction in 2010.

Office

Leeds’s sizeable financial and professional services sector, coupled with its growing reputation as a tech and media hub, has supported demand for office space and boosted confidence among market participants in recent years. While leasing has slowed since the pandemic started, there have been some sizeable transactions agreed in recent quarters, including one of the largest lettings in recent years, 138,500 SF to Lloyds Bank at 11-12 Wellington Place.

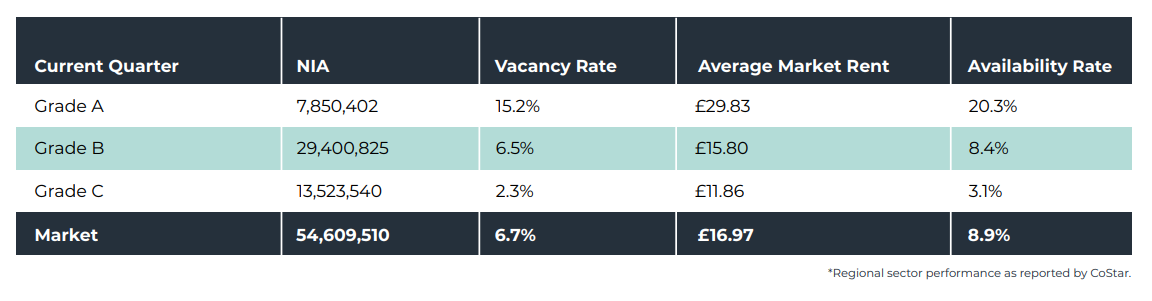

Although vacancies have crept up to 6.7% amid occupiers’ consolidation (and are expected to rise further with negative net absorption), CoStar’s Base Case forecast scenario calls for them to remain below those of other Big Six office markets and the UK overall. The market’s demand base remains diverse, with technology, finance and professional services, education, the public sector and flexible workspace firms all involved in notable lettings over the past 12 months. Net absorption has, however, been negative in recent years, as firms have reduced their office footprints amid the shift to more flexible ways of working. Large blocks of space have been offloaded by companies in the public, finance and energy sectors.

Rising vacancy is putting downward pressure on rental growth, which has slowed to 1.5% year-over-year and is expected to fade further in the coming months in line with rising supply. Average office rents in Leeds (£17.00/SF) are among the lowest in the Big Six, and some developers have taken advantage of the upside potential of refurbishment projects, particularly in the City Core. Prime headline rents in the city centre stand at £37/SF, which is also lower than other Big Six office markets.

Investment into Leeds’s office market has cooled down since the onset of the pandemic, especially in recent months, in response to rising interest rates and debt costs. Yields are moving out, and annual volumes (£91.2 million) are down sharply on the £600 million invested in 2018 and 2019 and the market’s five-year annual average (£301 million). The largest transaction in over 12 months was agreed in August, providing an asset management opportunity, which is a recent trend. Artmax AB sold 1 Sovereign Street to Shakra Investments (a private Lebanese investor) for £38.7 million reflecting a net initial yield of 7.0%. The 139,079 SF building was purpose built for BT and is currently let at a low rent of £19.50/SF. The opportunity to drive rental is provided by RPI-linked rent reviews due in 2025 and 2030, as well as an opportunity through refurbishment.

*As reported by CoStar

Sign up to our mailing lists to stay up to date with the latest news here